Environmental risks play a crucial role in property transactions, and as conveyancers and solicitors, conducting thorough environmental searches is key to safeguarding your clients’ interests.

Our parent company Landmark has long been the trusted provider of comprehensive environmental search reports. Now, with their enhanced residential product portfolio, we cover all environmental risks included in every Landmark residential report—allowing you to choose the report best suited to you, from basic identification to full expert analysis.

In addition to providing a more flexible and thorough assessment, we’re excited to announce two major improvements: the inclusion of climate change modules in the Landmark’s EnviroSearch and RiskView reports, plus an innovative approach to coal risk assessment. These advancements ensure that you’re equipped to handle today’s environmental challenges more effectively than ever.

The key environmental risks every conveyancer should consider:

- Contaminated Land

- Flood

- Coal Mining

- Climate Change

- Planning

- Ground Stability

- Radon

- Energy & Infrastructure

- Planning Constraints

These risks can significantly impact property value, insurability and enjoyment of living in, what might be, your dream home. Landmark’s enhanced portfolio provides reports tailored to different levels of risk assessment, giving conveyancers the flexibility to choose the depth of analysis that best fits their needs.

Introducing the ‘coal revolution’: the new way of searching for coal risk

One of the most significant improvements in the new product line-up is the reimagined approach to coal risk assessments. With Landmark’s coal revolution, you can expect faster, more accurate and more comprehensive coal risk assessments. The symbiosis between alert and full assessments in the reports, combined with the added security of an equivalent to a No Search Required Certificate with £1 million indemnity, sets a new industry standard for coal mining risk assessments.

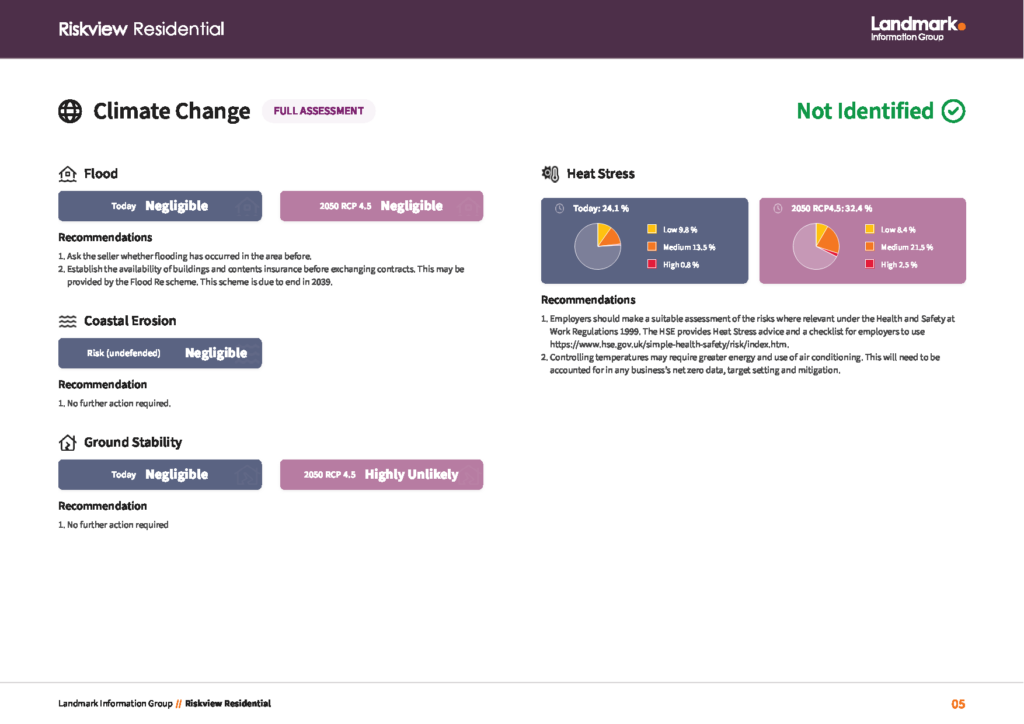

Climate Change: now included in EnviroSearch and RiskView

In response to increasing concerns about climate change, Landmark have also integrated their climate change modules into both Landmark EnviroSearch and RiskView products. These modules provide a forward-looking analysis of how climate change may impact a property over time, helping you and your clients understand potential long-term physical risks such as increased flooding, coastal erosion, as well as transitional risks such as energy efficiency of buildings. By incorporating climate change assessments, Landmark ensures that your due diligence is not just relevant for today but also for the future.

Landmark’s enhanced residential product portfolio: A closer look

Landmark’s enhanced suite of products is designed to meet the varied needs of conveyancers, from basic checks to detailed assessments. The three key products in this portfolio are:

- Homecheck Residential: This report provides an initial assessment across all key risks, identifying potential issues that may require further investigation. It offers an overview that helps you determine if more in-depth analysis is necessary and whether a supplementary report is needed.

- EnviroSearch Residential: This report offers a more detailed assessment, including the newly added climate change module. It provides a breakdown of risks and a full evaluation of each environmental peril, perfect for when more certainty is needed.

- RiskView Residential: The most comprehensive product, RiskView Residential, includes full data assessments and expert analysis through Landmark’s environmental consultants. With the addition of the climate change module, this product delivers the highest level of accuracy and foresight, ensuring that all risks are meticulously evaluated.

Using Flood Risk as an example: the same site, different experience

To demonstrate how these products differ in practice, let’s look at a typical scenario involving flood risk assessment:

Scenario: A Homebuyer has had their offer accepted and is eagerly waiting to arrange their move in date. Before this is possible, their conveyancer is reviewing their Environmental Search to see if there are any concerns to flag to the Homebuyer.

- Homecheck Residential: The report identifies that the property is in a flood-prone area, prompting further investigation. The assessment highlights potential risks but does not provide detailed specifics.

Report outcome – Identified

- EnviroSearch Residential: This report offers a full flood assessment, breaking down the risk by specific perils such as River, Coastal, Surface Water, and Groundwater. In this case, a high risk for surface water flooding is identified, and recommendations are provided, including whether the site is insurable under standard terms. This product also includes the climate change module, offering insights into how future environmental changes might impact the property from flooding.

Report Outcome – Further Action

- RiskView Residential: The RiskView report identifies the high risk of surface water flooding and refers the case to Landmark’s environmental consultants for expert evaluation. The consultants determine that the high-risk area is limited to an adjacent road, allowing them to downgrade the overall flood risk and provide a “Passed” outcome. Additionally, the climate change module helps evaluate long-term impacts, offering an even more comprehensive risk profile for the property and confirms the risk doesn’t worsen over time.

Report Outcome – Passed

Clarity & confidence: key benefits

These enhanced residential products offer the most comprehensive environmental reports on the market, presented in a format that’s easy to use and understand. Key benefits include:

- Comprehensive Coverage: Every report covers all key environmental risks, from coal mining to planning and everything in between, ensuring thorough due diligence.

- Clear Risk Assessment: The user-friendly format makes it easy for conveyancers and clients to understand the environmental risks and how they have been assessed.

- Enhanced Usability: The reports retain a fixed structure to keep them familiar from one case to the next. The intuitive layout and navigation throughout make locating information straightforward.

- Assessment Options: You can choose the level of detail required, with options ranging from basic checks to full expert analysis, including new features like the new innovative coal alert.

Comprehensive due diligence, made easy

Landmark’s new portfolio empowers you to provide your clients with the highest level of due diligence, helping them make informed decisions and avoid unpleasant surprises down the line. By addressing all key environmental risks in one report, you can confidently manage the complexities of environmental due diligence with ease.

Your next step

To learn more about how Landmark’s enhanced residential products and streamline your conveyancing process, download and review the Product Comparison Matrix and Toolkit today. These resources provide a side-by-side comparison of the different levels of risk assessment available, helping you make the best choice for your clients.

The original version of this article was originally published by Landmark Information Group. For more information from the full range of Environmental Insights remastered products available from OneSearch, click here.

Environmental insights are changing!

Our parent company Landmark Information Group are thrilled to share the launch of a remastered range of residential environmental search reports specifically designed to help you feel confident with search results, spend less time interpreting data and more time delivering excellent customer service.

Environmental Insights Remastered

Landmark’s remastered reports will still contain unmatched data and renowned in-house expert support but now with greater clarity, helping you navigate the most complex transactions, seamlessly.

Remastered content and design, led by conveyancers

To support these latest updates, Landmark engaged with over 200 residential conveyancers, from high street to multi practice firms; the invaluable feedback they provided together with Landmark’s 30 years of experience in property and land data, has allowed Landmark to remaster and shape environmental reports that properly satisfy the need for readability, comprehension and expediency.

Comprehensive due diligence, made easy

- New and upgraded risk modules to ensure we provide not only the most comprehensive reports in the market but the simplest way to convey environmental risk.

- Visually enhanced front pages – providing greater transparency for conveyancers to save valuable time.

- New executive summary pages for both conveyancers and homebuyers to understand quickly and easily which risks are relevant for that location and what to do next.

- Homebuyer guidance – to ensure your clients understand the report context.

Remastered Delivery

From the research Landmark carried out, PDF delivery is still extremely popular, but there was an awareness that digital formats will be the future moving forward. To support and prepare conveyancers with this transition Landmark’s remastered reports will be digitally enabled, giving choice on how you want to receive environmental insight information in the future.

To view the remastered catalogue, click the related products links below.

The potential dangers of contaminated land do not stand out to prospective purchasers when the door opens on the property of their dreams, spruced up and dressed for sale.

However, neglecting to investigate potential contamination on a property could spell trouble for buyers and the environment. Failing to conduct due diligence might mean hefty clean-up costs, health risks and legal issues for the new owners down the line. The spread of contaminants could harm not just the property but also the homes of neighbours and the local community.

It is the conveyancer’s responsibility to ensure home movers are fully aware of and safeguarded against the financial and environmental hazards associated with contaminated land.

The importance of due diligence

Bypassing environmental assessments to speed property transactions and reduce costs is both a false economy and dangerous. The Law Society notes:

“…you should consider in all conveyancing transactions whether land contamination is an issue.”

The only way to identify contaminated land issues is with an environmental search.

Should the environmental search expose contaminated land, the Environmental Protection Act applies the polluter pays principle, which aims to charge the original contaminator, but that is not always possible. There is strict liability on property owners for remediation costs, regardless of when the contamination occurred – even if the owner takes on the property decades after the contamination happened and the original contaminator cannot be found. Failing to disclose known contamination issues can also expose sellers and conveyancers to legal action for misrepresentation.

There are instances in which the costs for dealing with the contamination have exceeded a property’s market value, and that has plunged new private owners into negative equity and turn a dream forever home into a millstone. The importance of technical and legal due diligence regarding contaminated land cannot be understated. Where an environment search throws up a ‘Further Action’ on a property, it is on the conveyancer to dig deeper, to act further.

Article originally published by Landmark Information Group

The strong winds and torrential rains of Storm Babet made landfall on 18 October 2023. Storm Babet was named after a woman who visited a Dutch weather agency KMNI open day and asked for her name to be used “because [she] was born during a storm.”

Discover the Meteorological Insights

What was the human impact?

• 7 killed

• 2,146 properties flooded

• 100,000 people affected by power cuts

Most affected: East Scotland, Derbyshire, North Wales, County Cork.

Environment Agency (EA) confirmed 100,000 properties were protected with 20 high-volume pumps and five small-volume pumps deployed across several sites. EA’s flood warning service sent out over 300,000 messages by email, telephone and text during Storm Babet.

The impact on businesses

Inchcape JLR dealership in Derby, which opened in 2019 on the city’s former cattle market, closed due to damage

caused by the River Derwent flooding.

It was reported that despite Environment Agency concerns the “dealership would end up under two metres of water – or more – in a ‘one in 100-year’ flood,” Derby City Council had approved the development.

Landmark pulled an Argyll Environmental report on the dealership’s site, and the data is clear: the development site was at moderate to high risk of flooding with moderate groundwater, surface pluvial and other factors putting it at risk of flooding.

There is even considerable history of flooding in this location, which would make insuring the plot challenging– and certainly expensive.

Discover Landmark’s analysis of this site.

Article originally published by Landmark Information Group.

Our recent webinar ‘The Law Society Guidance on the Impact of Climate Change on Solicitors: What does this mean for solicitors?’ is now available to watch on demand.

The webinar, hosted by Landmark, focussed on The Law Society Guidance on the Impact of Climate Change on Solicitors, and was originally shown on the 4th May.

The webinar was specifically designed for solicitors as a tool to help them understand the guidance and its implications.

The session covers two main areas of the guidance.

- Firstly, reducing the climate change impact of the law firm and its clients, which includes assessing annual carbon emissions and setting targets to achieve net zero by 2050.

- Secondly, the guidance examines climate change risks, including the duties of advising and warning clients about such risks.

Our distinguished speakers are Kirsty Green-Mann, Head of Corporate Responsibility at Burges Salmon LLP, Professor Robert Lee at Birmingham University, and Simon Boyle, Environmental Lawyer at Landmark.

AGENDA:

- Summary of the Law Society Guidance and what this means for solicitors’ advice

- What’s the role that a law firm plays in reducing its carbon footprint and disclosing climate-related risks and opportunities?

- An overview of how Burges Salmon has implemented Net Zero

- Panel Discussion: What are the requirements for lawyers to fulfil the guidance and next steps for them

- Q&A

To watch the webinar on demand, please visit this page, and fill in the form.

This survey and guide reveals how a desire for more information about climate and the environment may start changing residential conveyancing processes.

The transition to Net Zero is a long term goal, but it’s clear home movers are factoring climate change into their decisions now. Our parent company Landmark’s survey shows there’s already a desire for more data, earlier in the process. It’s a revealing snapshot.

Download the guide to find out:

- Residential conveyancers views on who is responsible for advising on climate change

- The percentage of home movers prepared to invest in energy efficiency measures

- How agents and conveyancers are handling the need for a Net Zero strategy

- What percentage of firms are reporting on future climate change risks to their clients

Residential estate agents and conveyancers are trusted to source the right information at the right time. This survey shows that many firms want more guidance from authoritative organisations on the provision of climate change information to home movers.

Landmark Information Group provides climate data to colleagues working in every part of the property industry’s value chain. Our work includes surveys and reports like this one, surfacing insights on subjects such as Climate Change, Digital Transformation, and the Home Mover Experience.

Download the guide, understand colleagues’ views on reporting around climate change and information exchange with vendors and purchasers.

Complete the form, we’ll send our guide – View on Climate Change Information in Residential Conveyancing – straight to your in-box.